Every US recession in the last 50 years has been preceded by an inversion of the US yield curve. This much-followed market indicator has infamously predicted nine of the last six recessions, but even with the false positives it is a phenomenon that cannot be ignored. In March, the Federal Reserve raised interest rates for the first time since 2018; by the end of the month, the curve had briefly inverted intra-day. It was back in an inverted position at the start of this week.

Past performance does not predict future returns. You may get back less than you originally invested. Reference to specific securities is not intended as a recommendation to purchase or sell any investment.

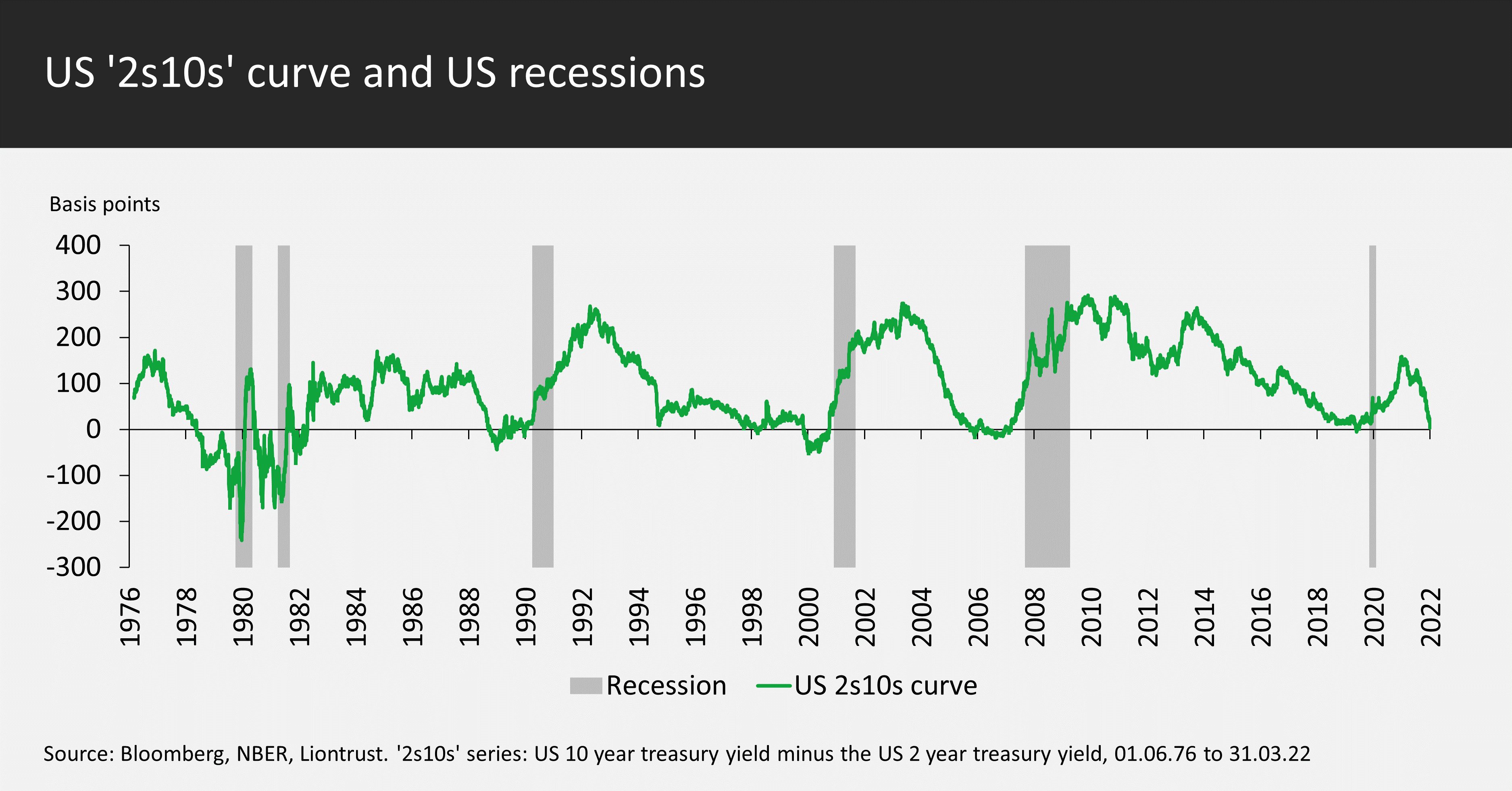

Firstly, for those not familiar with bond market jargon, the yield curve merely represents the difference in yields between bonds of varying maturities. Normally, yield curves are upward sloping; it is riskier to lend to the government for longer periods as the chance of inflation eroding the value of your bond investment goes up, as does the risk of a deterioration in the credit quality, or even of a default. The specific part of the yield curve studied as a recessionary indicator is the US 2s10s: the difference in yields between the US 10-year government bond and 2-year Treasuries. An inversion is when the latter yields more than the former.

I should note that others prefer to look at 3-month yields compared to the 10-year. The two generate similar results but the 2s10s is more forward looking. On average, it takes about 18 months after the 2s10s yield curve inverts before a recession starts, but there is a large variation around the timing. There is less of a lag between any inversion of the 3-month versus 10-year yield differential and a recession occurring – this just shows that policy had become too tight (interest rates are too high and have choked off growth and investment). Presently, the curve between 3 months and 2 years in the US is very steep; effectively telling you that the Federal Reserve is hugely behind in this cycle and will be increasing interest rates rapidly to try to catch up.

I should note that others prefer to look at 3-month yields compared to the 10-year. The two generate similar results but the 2s10s is more forward looking. On average, it takes about 18 months after the 2s10s yield curve inverts before a recession starts, but there is a large variation around the timing. There is less of a lag between any inversion of the 3-month versus 10-year yield differential and a recession occurring – this just shows that policy had become too tight (interest rates are too high and have choked off growth and investment). Presently, the curve between 3 months and 2 years in the US is very steep; effectively telling you that the Federal Reserve is hugely behind in this cycle and will be increasing interest rates rapidly to try to catch up.

During March, various Federal Reserve speakers voiced opinion that the pace of tightening must accelerate, with the consensus now saying that interest rate policy has to get beyond neutral or even to tight levels in order to bring inflation under control. Explicitly, the Fed’s median dot plot policy rates predictor is now 2.8% versus its estimate of a 2.4% neutral level (we discussed the hawkish rate rise during March). The problem is that inflation has become embedded in expectations, with wage inflation being the most important self-fulfilling inflationary feedback loop.

The Fed has its own preferred measure (the 18-months forward 3-month rate minus the current 3-month rate), but all it currently shows is that the Fed should not have left policy so loose for so long – we have been vocal in that regard since early 2020. More interestingly, officials were keen to talk about the prospect for an economic soft landing, such as that achieved in 1994. The bond market clearly disagrees, as you can see from the narrowing of the spread between 10-year and 2-year yields in the chart above (a flattening of the yield curve), before the yield curve’s inversion. So, is it “different this time?”

The Fed has its own preferred measure (the 18-months forward 3-month rate minus the current 3-month rate), but all it currently shows is that the Fed should not have left policy so loose for so long – we have been vocal in that regard since early 2020. More interestingly, officials were keen to talk about the prospect for an economic soft landing, such as that achieved in 1994. The bond market clearly disagrees, as you can see from the narrowing of the spread between 10-year and 2-year yields in the chart above (a flattening of the yield curve), before the yield curve’s inversion. So, is it “different this time?”

Whilst the yield curve would probably be steeper without QE, the flattening of the last 3 months cannot be ignored.

There is an argument that quantitative easing (QE) has depressed the term premium, the extra yield one should be paid for owning longer maturity government bonds. I have some sympathy with this but would counter that QE has also kept short rates too low. Whilst the yield curve would probably be steeper without QE, the flattening of the last 3 months cannot be ignored. This is particularly the case as we rapidly approach the period when quantitative tightening (QT) will start.

Although interest rates were much higher half a century ago, there is strong similarity with the experience in the 1970s in that the curve currently is inverting as we witness a supply shock. Firstly, the pandemic constrained supply and, post the great economic reopening, there are still bottlenecks throughout the supply chain including, for example, for semiconductors. Now Putin’s war has caused further spikes in commodity prices. These will continue to feed into headline inflation over the months to come. But will they feed into core inflation in the longer term? For this we need to look at the demand side of the equation.

The consumer is in a fortunate position of having a strong balance sheet, with excess savings having accrued during the pandemic lockdown periods. These savings are not distributed equally, with socio-economic groupings A to C owning the vast majority. Thus, it is the lower socio-economic groups that not only lack savings but also have a higher exposure to headline inflation through the necessity of heating and eating; such basics are frequently excluded from core inflation calculations. The wallet substitution impact of higher energy prices can be mitigated in two ways, government intervention (with huge variance country by country) or by wage inflation. Labour markets are tight and elevated wage inflation remains our central case for the next couple of years – hence why central bankers are having to act.

For some time, we have believed that economies are comfortably strong enough to live with interest rates being higher for longer, especially if they curb inflation and actually improve living standards. This is on the basis that, for example, the Federal Reserve raises rates to the 2% area and keeps them there, rather than raise more aggressively only to cut in short order. With some Fed voting members now wanting rates above 3% the goalposts have shifted and there is a real danger rates are now raised to recession-inducing levels.

So, to answer whether it will be different this time: if the Fed rapidly raises interest rates to be above 3%, then we think a recession is likely to follow in 12-24 months’ time (so, no, it is not different this time); if, however the Fed is partly just talking a hawkish game to discourage inflation expectations and pauses at 2%, then we will expect a soft landing and the yield curve to start steepening again.

Understand common financial words and terms

See our glossary

Key Risks

Past performance is not a guide to future performance. The value of an investment and the income generated from it can fall as well as rise and is not guaranteed. You may get back less than you originally invested. The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

Investment in Funds managed by the Global Fixed Income team involves foreign currencies and may be subject to fluctuations in value due to movements in exchange rates. The value of fixed income securities will fall if the issuer is unable to repay its debt or has its credit rating reduced. Generally, the higher the perceived credit risk of the issuer, the higher the rate of interest. Bond markets may be subject to reduced liquidity. The Funds may invest in emerging markets/soft currencies which may have the effect of increasing volatility. Some of the Funds may invest in derivatives. The use of derivatives may create leverage or gearing. A relatively small movement in the value of a derivative's underlying investment may have a larger impact, positive or negative, on the value of a fund than if the underlying investment was held instead.

Disclaimer

This is a marketing communication. Before making an investment, you should read the relevant Prospectus and the Key Investor Information Document (KIID), which provide full product details including investment charges and risks. These documents can be obtained, free of charge, from www.liontrust.co.uk or direct from Liontrust. Always research your own investments. If you are not a professional investor please consult a regulated financial adviser regarding the suitability of such an investment for you and your personal circumstances.

This should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. The investment being promoted is for units in a fund, not directly in the underlying assets. It contains information and analysis that is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content of this document, no representation or warranty, express or implied, is made by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified. It should not be copied, forwarded, reproduced, divulged or otherwise distributed in any form whether by way of fax, email, oral or otherwise, in whole or in part without the express and prior written consent of Liontrust. Always research your own investments and if you are not a professional investor please consult a regulated financial adviser regarding the suitability of such an investment for you and your personal circumstances.