Tactical Asset Allocation (TAA) is one of the five stages of the Multi-Asset investment process – the others being Strategic Asset Allocation (SAA), fund selection, portfolio construction and monitoring.

The Multi-Asset investment team has a medium term view – 12 to 18 months – of the prospects for each asset class and this forms the TAA. Each asset class is assigned a rating from one to five, with one most bearish and five most bullish. TAA is the target (not the actual position) for every asset class and the investment team builds towards this within the funds and portfolios over time. Having a 12 to 18-month view means the team will increase positions when the valuations of the asset classes are attractive; their core approach is to buy low and they will not overpay for assets, however highly they score.

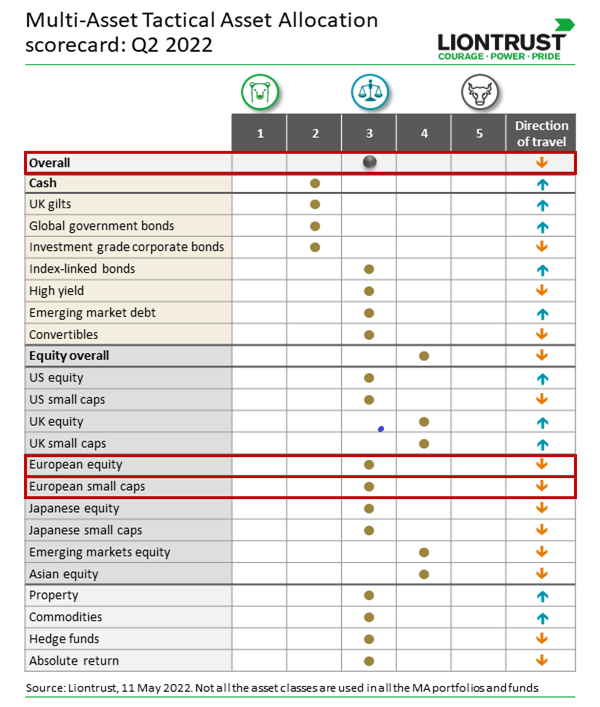

The team reviews TAA every quarter but it is important to stress this does not reflect a quarterly view. The rating is only altered up or down when there is a fundamental change in the assessment of a particular asset class, and by taking a longer-term view, the team is seeking to ignore short-term market noise and avoid trying to time the market. The table above shows the latest TAA and includes all asset classes regardless of whether they are included across the funds and portfolios. The direction of travel arrow shows the last change in the TAA, whenever this occurred.

Changes in this latest version (highlighted in red) are fairly small, although our overall ranking on markets has come down from four to three. We remain positive but this change acknowledges current challenges in terms of inflation and growth and the team feels the backdrop has become one where it is prudent to rein in portfolio risk slightly.

Elsewhere, our ranking on European equities and European smaller companies has also fallen from four to three. Again, we stress this remains a positive score but Europe is the region most at risk from the current war in Ukraine, with all the geopolitical fallout and sanctions that may bring.

While slightly less positive overall, our rankings on individual asset classes have remained unchanged as we see similar fundamentals and opportunities in place.

|

Asset class |

Q2 2022 Score |

Direction of travel |

Commentary |

|

Overall |

3 |

↓ |

As stated, we have moved our overall score down from four to three but would say we are actually more at 3.5, reflecting the fact navigating higher inflation and slowing growth calls for slightly more defensive positioning. We feel risks to the downside are more prevalent than in previous quarters, so the lower ranking is warranted. Beyond geopolitics and ongoing outbreaks of Covid, particularly in China, the key questions this year and beyond are when we will see peak hawkishness from central banks and how successfully they can engineer a soft landing while also curbing runaway inflation. We continue to believe inflation should start to fall in the second half of the year as the rolling base effects from Covid shutdowns work their way through the system. That should allow central banks to tread carefully and be less aggressive on the hiking front than markets are currently predicting but there also remains a risk of policy surprise or unintended consequences, neither of which are supportive for markets. Concerns are also rising around slowing growth but we feel a technical, ‘small R’ recession (two consecutive quarters of negative growth) is more likely than a ‘real’ recession, where a protracted slowdown emerges. While current newsflow is broadly negative, equity markets remain attractively valued, particularly after recent indiscriminate selling. The UK is still cheap despite the recent energy rally and value rotation, for example, and even the US is less unattractive after two corrections (falls of 10% or more) in the S&P so far this year. Within bonds, we appreciate the direction of yields will be upward over time (as interest rates climb) but, as ever, the path will not be linear and we maintain exposure to this asset class for its long-term diversification to equities, some level of inflation protection and increasing income. For now, we retain a lower duration position in our fixed income allocation as central banks prevaricate over the timing and extent of rate rises and tapering. |

|

Cash |

2 |

↑ |

Cash remains a broadly unattractive asset class but we moved the ranking up to two in Q1 to reflect the fact that, on a relative basis, it looks better as a store of value in a rising interest rate environment. Compared against duration assets such as government bonds, for example, where rising yields will erode capital values, there is a stronger argument for cash, although it is obviously hit by higher inflation. |

|

UK gilts |

2 |

↑ |

Yields have risen sharply, with the Bank of England’s (BoE) Monetary Policy Committee now four hikes through its cycle as it looks to bring inflation under control. Despite its actions so far, there is a sense the BoE has moved from the most hawkish of central banks to a more hesitant hiker, more cognisant of macro risk than some peers. Yields on 10-year gilts have risen from around 0.7% at the start of December to above 1.8% today and could continue to climb in line with base rates. If they get to 2.5%-3%, that would represent a more attractive opportunity. For now, we moved slightly less negative on gilts in Q2 2021 but this asset class remains underwhelming, with the bias of risk still to the upside for yields (or the downside in price terms), especially if higher inflation persists. Gilts still provide a useful function as portfolio insurance in times of market duress but offer little more than a cushion to equities. |

|

Global government bonds |

2 |

↑ |

A global basket of currencies and interest rate risks can result in a differentiated return stream from UK gilts. Again, yields have increased and could climb higher, and for now, the bias of risk remains to the upside (or downside in price terms), especially if higher inflation persists. While there is some diversification benefit versus the UK in terms of interest rate policy, as stated, the BoE looks be moving less hawkish as it tries to maintain the balance between reducing inflation and not tipping the economy into recession. Again, these bonds still provide a useful function as portfolio insurance in times of market duress but offer little more than a cushion to equities. |

|

Investment grade (IG) corporate bonds |

2 |

↓ |

We moved our ranking on investment grade credit back from three to two last quarter, in recognition that spreads had narrowed and no longer offered as much cushion for the additional credit risk.

Spreads have now moved out to 2019 levels and there is a risk they could go wider in the event of a significant recession. Yields to worst levels in the 3% range for UK investment grade and 4% for US are starting to look more interesting. Looking against gilts, there is a case for investment grade but we feel the asset class still remains less compelling versus recent history. |

|

Index-linked bonds |

3 |

↑ |

This debt will benefit versus nominal government bonds if inflation continues to run ahead of expectations, although higher levels look to be reflected in elevated prices. Index-linked bonds tend to have longer duration than the same tenor nominals so duration positioning needs to be considered. It is best to buy inflation protection when the risk is underappreciated, which is certainly not the case today. |

|

High yield (HY) |

3 |

↓ |

Again, spreads have moved out to 2019 levels and there is a risk they could go wider in the event of a significant recession. Yields to worst levels in the 7% range for US high yield look interesting but there is more risk of bankruptcy in this market, especially if conditions worsen, so more cautious and active managers are recommended. |

|

Emerging market debt (EMD) |

3 |

↑ |

Hard currency yields to worst levels are around the same as high yield at present: on the positive side, credit ratings in EMD are generally superior to HY, whereas on the negative, the Russia situation shows the political risk inherent in these markets. Our view remains that while spreads look reasonable, the idiosyncrasies of the emerging market environment are potentially better rewarded in EM equities. |

|

Convertibles |

3 |

↓ |

We continue to see convertibles as providing an attractive risk/return profile thanks to their optionality and bond floor. Our view moved down from four to three in Q4 2021 as we took profits after a strong spell of performance and feel the asset class has potentially peaked for this cycle. |

|

Equities overall |

4 |

↓ |

While our overall score has fallen to three, equities remain a four and we see most markets overall as attractively priced, particularly after indiscriminate selling over recent weeks. The obvious risks lie in tightening monetary policy and slowing growth but there is a sense share prices, via corrections, have already factored in worsening prospects for 2022. That said, we expect returns to be lower than seen in the recovery since the sharp Covid shock back in March/April 2020. Amid an ongoing value rotation, growth stocks, particularly in the US, have fallen into a bear market, with two 10%-plus corrections in the S&P 500 already this year, which offers the opportunity to top up growth and quality holdings. We have seen the US as prohibitively expensive for much of the last decade and while still not attractive, it is certainly less unattractive after these corrections. Elsewhere, we continue to favour markets such as the UK, which is still cheap despite a strong run this year. In a reflationary environment, we expect the rest of the world to outperform the US, value stocks to outperform growth and small caps to outperform large. These outperformances will not all come at once, however, so we retain prudent diversification rather than making a significant gamble that one particular thesis pays off. |

|

US equity |

3 |

↑ |

We have long been cautious on the expensive US but recent corrections have brought valuations back to more sensible, and less unattractive (if not quite yet attractive), levels. Looking forward, there are a few points to consider: the US has experienced a tech bear market that has taken some of the froth out of the growth end of the market, which may create opportunities; but an inflationary period does not typically support growth (or long-duration) stocks, which the US continues to have in abundance. Value can still be found beneath the tech behemoths and the US economy remains in relatively solid shape, potentially benefiting from its isolation in terms of energy policy and agriculture. Overall, history suggests returns from the S&P are likely to be lower in 2022, with performance after a 20%-plus year tending to sit around 8%. While valuations are looking more attractive and long-term earnings should be solid, active exposure is still definitely warranted, with rotation of styles a risk to market cap weighted indices. |

|

US small caps |

3 |

↓ |

Our ranking on US smaller companies fell from four to three last quarter, bringing it back in line with the overall US market. Smaller companies have suffered in recent selloffs but, longer term, we continue to believe in the small-cap premium and the short-term re-rating could give us a buying opportunity. Overall, smaller companies in the US should benefit from the same broad themes as the large-cap market with additional sensitivity to domestic economic conditions, whether positive or less so. |

|

UK equity |

4 |

↑ |

UK equities remain cheap despite the recent energy bounce and the overall skew to value. The UK has outperformed other developed markets so far this year but there is still a long way to go, particularly if the value rotation continues: financials, for example, should benefit from a more forgiving yield curve and higher prevailing yields than we have seen for many years. |

|

UK small caps |

4 |

↑ |

As in the US, smaller companies have suffered amid recent selloffs but, longer term, we continue to believe in the small-cap premium and the short-term re-rating could give us an opportunity. Overall, smaller companies in the UK should benefit from the same broad themes as the large-cap market with additional sensitivity to domestic economic conditions, whether positive or less so. |

|

European equity |

3 |

↓ |

While Europe remains attractively valued, we have moved the score down from four to three this quarter. Europe is the region most at risk from a protracted conflict in Ukraine, with all the geopolitical fallout and sanctions that may bring. Parts of the bloc are heavily reliant on Russian energy and the transition away from that will likely prove painful. In addition, while the European Central Bank (ECB) looks set to remain on the more dovish side, its one-size-fits all approach to policy means there is greater risk of inflationary hotspots. As in the Global Financial Crisis, the ECB has to act unilaterally and has little room for nuance, meaning prevailing policy could be inappropriate for large parts of the Continent. Finally, Europe is heavily dependent on exports so more sensitive to the global economic cycle and any risk of slowdown. |

|

European small Caps |

3 |

↓ |

As above, and for the same reasons, we have downgraded European small caps for four to three, based on that risk of recession and inflation overshoots in certain countries if the ECB is reluctant to move aggressively on interest rates. |

|

Japanese equity |

3 |

↓ |

Our conviction on Japan has fallen over recent quarters (from four to three) but while the market has sold off in line with others year to date, it is largely unaffected by prevailing geopolitical risks. Where current conditions may impact the region is as a market reliant on exports (although yen weakness may be positive here), and, as with Europe, softening global growth could be problematic. The country’s central bank is also sitting outside the hawkish camp for now, with rates expected to stay low, and it remains to be seen whether this period results in some imported inflation (after decades of deflation) and how the country’s conservative consumers react to that. |

|

Japanese small Caps |

3 |

↓ |

Again, smaller companies in Japan should benefit from the same broad themes as the large-cap market with additional sensitivity to domestic economic conditions, whether positive or less so. |

|

Emerging markets equity |

4 |

↓ |

Emerging markets should continue to benefit from the global reflation trade, with loose monetary policies and a weak US dollar providing a supportive environment. While long-term positive fundamentals remain intact, shorter-term pandemic shocks and recent policy shifts, both centred on China, have hit sentiment. The country looks to have avoided renewed lockdowns but Chinese stocks on the CSI 300 dropped to their lowest level in two years in April as the government shut areas of Beijing and ordered mandatory Covid testing in one district. This came after China’s central bank unveiled a suite of measures designed to support the economy and billions in yuan wiped off stock prices over the month was clearly not in the script. EM equities remain highly geared into sentiment shifts – both positive and negative – and are also sensitive to domestic and international politics. |

|

Asian equity |

4 |

↓ |

As with EMs, Asia is benefiting from the reflation trade and loose monetary policies and a weak US dollar provides a supportive environment. These economies have, on the whole, fared well through Covid but a lot clearly rests on China and how it supports its economy in the months ahead. Risks remain from the perspective of global sentiment as well as regional political tensions, although Asia has performed well recently thanks to its commodity links. |

|

Property |

3 |

↑ |

Property still offers a reasonable yield pick-up compared to other asset classes, as well as some protection against inflation. However, there is also uncertainty surrounding several property types in a post-Covid world: the anticipated demise of the office and high street retail sectors could be overstated but current pressures on tenants will have long-term repercussions. We tend to favour more specialist parts of the property market enjoying structural growth, such as healthcare, logistics and digital infrastructure. |

|

Commodities |

3 |

↑ |

Commodities have rebounded strongly off their lows and are not as attractive a value play today, although the situation with Russia and Ukraine has created short-term volatility in the oil price. Over the medium to long term, they should remain correlated to global economic activity. Broad allocations to commodities should also provide some protection if inflation surprises on the upside. Conversely, downward price pressure could resume if growth disappoints. |

|

Hedge funds |

3 |

↓ |

Given time, the right hedge fund strategy can provide a diversified return stream compared to more traditional asset classes. These funds are unlikely to keep up with a raging bull market but should post reasonable returns in a constructive environment for risk assets. We have recently moved towards real assets in our ‘alternatives’ allocation, which also offer an element of inflation protection. |

|

Absolute return |

3 |

↓ |

Well-chosen absolute return vehicles can be a useful diversifier to overall portfolio risk thanks to their low correlation with traditional asset classes. But they are unlikely to keep up with ultimate safe havens such as government bonds in times of market duress. We have recently moved towards real assets in our ‘alternatives’ allocation, which also offer an element of inflation protection. |

Key Risks