The Liontrust GF Strategic Bond Fund returned -5.5%* in US dollar terms in September. The average return from the EAA Fund Global Flexible Bond (Morningstar) sector, the Fund’s reference sector, was -3.4%.

Market backdrop

US Federal Reserve sets the tone: A combination of strong US employment data at the start of the month and inflationary data coming in above already elevated expectations helped to catalyse negative returns for government bonds and riskier assets during September.

US headline CPI came in at an annual rate of 8.3%, above consensus forecasts of 8.1%. Similarly, core CPI of 6.3% was also 0.2% above expectations. It is the services component within CPI that caused the majority of the overshoot. Specifically, it was the “shelter” category that created the biggest upside surprise with primary rents up 0.74% month-on-month, and owner equivalent rents (OERs) up 0.71%. The impact of this sticky shelter inflation is something we have been discussing since late 2021, albeit we did not think it would get above about a 5% annualised rate (compared to the current 6.3% rate). It will remain elevated until later this year, or possibly Q1 2023, but then start to fade away after that. This is due to the lags that exist between prior house price rises and the shelter inflationary numbers; with US housing activity dramatically slowing this year (prime mortgage rates reached 6.8% at the end of September) the aforementioned fading away is mathematically inevitable. The problem is that other components are elevated too, so pressure remains on the Federal Reserve to continue tightening monetary policy and it has shown it will keep hiking rates until aggregate demand is constrained enough for inflationary pressures to ease.

Therefore, it came as no surprise to see the Fed raise rates by 75bps for the third time in a row. The latest Summary of Economic Projections (SEP) contained some interesting information. There was an update to the dot plots - these are the representation of where the FOMC members see Fed funds rates being over coming periods. For the rest of this year it is a close call between 100bps and 125bps more tightening, with the latter just edging the consensus. This suggests the Fed will do one more 75bps hike at the start of November and then a 50bps one in December. 2023 has a reasonably well clustered consensus, with marginal further tightening anticipated. Cuts are predicted by 2024 and also in the newly introduced 2025 projections. For the very long term there was no change to what is viewed as a neutral level, nor should there be.

Part of the cause of the disparity in years further out is that the Fed is “discovering” what appropriate rate levels are; obviously monetary policy works with a lag so the Fed will want to see the impact of the cumulative official tightening, as well as that done on its behalf by changing market conditions. The SEP also offered up a few key highlights: inflation (core PCE) is now anticipated to be 3.1% in 2023, versus a prior 2.7% forecast; the 2024 estimate is unchanged at 2.3% and 2025 has been introduced at 2.1%. Unemployment in 2023 is now expected to be 4.4%, compared to the 3.9% forecast in June’s projection. GDP forecasts for 2023 have been revised down from 1.7% to 1.2%. It seems that Powell has low confidence in the GDP figure as there is an admission that the Fed is prepared to generate a recession to conquer inflation.

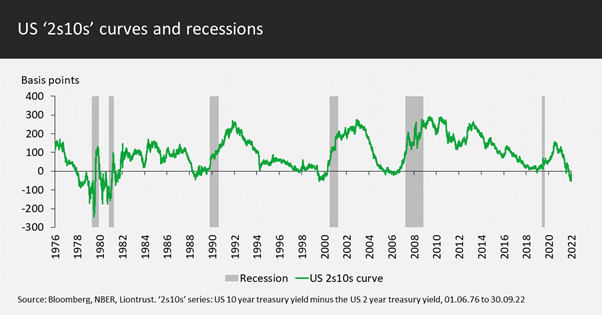

The market has been suggesting this would be the likely outcome since April this year when the yield curve inverted (10-year yields moving lower than 2-year yields). As illustrated by the chart below, the 2s10s curve is the most inverted it has been this millennium. With the move having been a bear flattening (all yields are higher, but short-dated have risen by much more than long dated ones), it is a good time to be adding some duration to funds.

The bond market’s interpretation of the inflation data and the Fed’s reaction function has been very interesting in September. As per the chart, the US Treasury yield curve has inverted further, with short-dated yields continuing to rise relative to longer-term ones. US 10-year bond yields increased from 3.2% to 3.8% during September, inflation breakevens compressed from 2.5% to 2.2%; thus, there was a huge jump upwards in real yields, which finished September just below 1.7%. This implies that the collective wisdom of the markets presently is that the Fed will be able to tackle inflation, but inflicting economic pain is necessary to achieve this. After all, if most of the inflation is now being driven by the demand side of the economy, central banks know they can hurt demand if they keep tightening policy. The higher CPI numbers and stickier inflation therefore mean that the terminal rate (peak rate in this cycle) will have to be higher to create the demand destruction and the risk of an ensuing recession continues to grow. The good news is that currently in the bond markets’ collective eyes the Fed has regained its hawkish credentials; the bad news is the economic damage the Fed is going to have to cause to follow through on getting the metaphorical inflation genie back in the bottle.

UK “fiscal event” creates credibility issue: It was a tough enough month for the bond markets prior to the UK’s fiscal event on the 23rd September. The economic illiteracy displayed caused contagion throughout developed markets. The main reason markets were spooked is that Kwarteng/Truss put the UK’s debt metrics on an unsustainable trajectory. The discarding of factors such as using the Office for Budgetary Responsibility only adds to the fears that the UK’s current Conservative government will dogmatically run roughshod over any UK institutions which usually provide checks and balances to further their ideology. Of course, I am a fan of tax cuts (who isn’t), but they have to be properly budgeted for and not at a time of already rampant inflation. There has been a U-turn so far on abolishing the 45% additional tax rate and one should expect that Kwarteng/Truss will try to restore some fiscal credibility by announcing huge spending cuts.

The UK’s Q2 current account balance reduced to a 5.5% deficit, still a level that requires constant inflows of international capital to finance the UK’s excess consumption (compared to production). This is why Mark Carney, former Governor of the Bank of England, once stated that the UK relies on the “kindness of strangers”. Over the next two quarters, the current account deficit is likely to reach 8-9% of GDP as UK imports of energy increase throughout the winter season.

Capital inflows into the UK can continue as long as investors/buyers have confidence in the quality of the UK’s institutional framework and legal system. The additional risk to UK solvency is now a factor to consider. To be clear, Truss/Kwarteng might have put the UK on a fiscally unsustainable path, but it is still highly likely that the trajectory is altered long before it becomes a fait accompli. The rise in gilt yields shows the extra price needed to fund the government’s profligacy. With bond vigilantes reasserting their authority, Truss and Kwarteng will rapidly find that what might sound good to Party members is not tolerated by international capital markets. The rapid rise in yields also had dramatic implications leading to intervention by the Bank of England.

Bank of England intervention due to margin calls: It is important to separate the policy responses of the Bank of England into the respective categories of targeting inflation and ensuring financial stability. The Truss/Kwarteng fiscal package is short-term stimulatory (but long-term negative as it is just a debt-funded splurge with a low multiplier impact and huge other ramifications), so the Bank of England will have to raise rates more than previously expected to tackle inflation. Bailey had a chance to make a between meeting hike, which would have sent a very strong message about the seriousness of the situation and helped earn him back a smidgeon of credibility. Unfortunately he blinked and pushed it back to the 3rd November MPC meeting. Pill (chief economist of the BoE) has since been talking a very hawkish game about being prepared to hike rates by as much as necessary, and the market has an increase of over 100bps priced in for the November meeting.

So why did the Bank of England restart up to £65bn of quantitative easing (QE) on the 28th September? In two words – margin calls. The solvency of the whole of the LDI (liability-driven investment) pension fund industry was called into jeopardy by the rapid rise in gilt yields, which was creating a self-fulfilling negative feedback loop. As a quick reminder: LDI has been all about reducing the risk of a funding shortfall for pension funds; long-dated liabilities (the anticipated pensions of the scheme members) are matched with appropriate assets. What a lot of LDI pension schemes have done is invest in short to medium-term assets and use a derivative overlay via interest rate swaps to match the long-dated liabilities. To put some context of the size of the exposure, Aon estimates that a £1bn pension scheme would have a DV01 of about £2m; the counterparty to this exposure is predominately investment banks. DV01 represents the profit or loss created by a one basis point move in yields; it is calibrated such that the impact on assets and liabilities matches. So, the margin call on the swaps of a 100bps rise in long-dated Gilt yields for a £1bn pension scheme is about £200m. The schemes have a pool of collateral that can be used to meet any margin call requirements when the profit/loss on the interest rate swaps changes, but when there is an outsized move in yields they might find themselves having to sell more of their illiquid assets. The problem was the combination of the speed and size of the move higher in gilt yields. LDI schemes simply could not raise collateral quickly enough; furthermore, the forced selling was exacerbating market moves. So, to emphasise, the liabilities of LDI pension funds have fallen in value by the same amount as the assets; the solvency issue is one of liquidity as opposed to a shortfall in assets. The Bank of England’s intervention is not about determining the yield on longer-dated gilts over the coming quarters and years, it is about ensuring an orderly market and stopping the doom loop of forced selling by LDI schemes.

Given that they are expanding their balance sheet again, the Bank of England has delayed the start of £80bn of quantitative tightening (QT) until 31st October. It is likely to view the £65bn extra as separate from the current stock of QE; it can therefore be unwound once market conditions permit. The intervention to create an orderly market may well help sway some of the MPC members to raise rates more rapidly to tackle inflation and this is one of the reasons for the markets’ expectation for a hike of at least 100bps on November 3rd.

Fund positioning and activity:

Rates

The large rise in bond yields during September created a valuation opportunity for us to take the Fund to a long duration stance. This was the most significant change to fund positioning during the month. We averaged in during September, adding the final 0.25 years’ increment when 10-year US Treasury yields were above 4%, finishing the month with a duration of 5.25 years. As a reminder, the Fund’s permitted range is 0 to 9 years and neutral is 4.5 years. The geographic duration split has US duration at 2.5 years, Europe 1.5 years, UK 0.9 years, and New Zealand 0.3 years. We continue to prefer the 5 to 10-year maturity parts of the yield curve.

Allocation

The Fund’s asset allocation was unchanged during September. Investment grade corporate bonds represent just under 60% of the fund’s assets. The high yield weighting remains slightly below 30%, above our neutral 20% level but below the 40% maximum. As a reminder, we have a large quality bias within this, limited exposure to the most cyclical parts of the credit market, and the Fund owns no CCC rated bonds.

Selection

As part the duration increase, we bought a couple of short-dated sterling-denominated bonds where yields have reached compelling levels. Specifically, senior debt with a 2027 maturity in HSBC and senior 2026 notes in Santander UK. The latter was a switch out of Santander’s dollar-denominated US entity bonds. Holdings in Singtel Optus and LSE, both denominated in euros, were trimmed due to being relative outperformers.

Discrete 12 month performance to last quarter end (%)**:

Past Performance does not predict future returns

|

|

Sep-22 |

Sep-21 |

Sep-20 |

Sep-19 |

|

Liontrust GF Strategic Bond B5 Acc |

-15.7 |

3.2 |

6.4 |

7.4 |

|

EAA Fund Global Flexible Bond - USD Hedged |

-12.1 |

4.3 |

3.4 |

6.7 |

*Source Financial Express, as at 30.09.22, total return, B5 share class.

**Source Financial Express, as at 30.09.22, total return, B5 share class. Discrete data is not available for ten full 12-month periods due to the launch date of the portfolio (13.04.18).

Fund positioning data sources: UBS Delta, Liontrust.

†Adjusted underlying duration is based on the correlation of the instruments as opposed to just the mathematical weighted average of cash flows. High yield companies' bonds exhibit less duration sensitivity as the credit risk has a bigger proportion of the total yield; the lower the credit quality, the less rate-sensitive the bond. Additionally, some subordinated financials also have low duration correlations and the bonds trade on a cash price rather than spread.

Key Features of the Liontrust GF Strategic Bond Fund

KEY RISKS

Past performance is not a guide to future performance. The value of an investment and the income generated from it can fall as well as rise and is not guaranteed. You may get back less than you originally invested.

The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

Investment in Funds managed by the Global Fixed Income team involves foreign currencies and may be subject to fluctuations in value due to movements in exchange rates. The value of fixed income securities will fall if the issuer is unable to repay its debt or has its credit rating reduced. Generally, the higher the perceived credit risk of the issuer, the higher the rate of interest. Bond markets may be subject to reduced liquidity. The Funds may invest in emerging markets/soft currencies which may have the effect of increasing volatility. Some of the Funds may invest in derivatives. The use of derivatives may create leverage or gearing. A relatively small movement in the value of a derivative's underlying investment may have a larger impact, positive or negative, on the value of a fund than if the underlying investment was held instead.

DISCLAIMER

This is a marketing communication. Before making an investment, you should read the relevant Prospectus and the Key Investor Information Document (KIID), which provide full product details including investment charges and risks. These documents can be obtained, free of charge, from www.liontrust.co.uk or direct from Liontrust. Always research your own investments. If you are not a professional investor please consult a regulated financial adviser regarding the suitability of such an investment for you and your personal circumstances.

This should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. The investment being promoted is for units in a fund, not directly in the underlying assets. It contains information and analysis that is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content of this document, no representation or warranty, express or implied, is made by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified. It should not be copied, forwarded, reproduced, divulged or otherwise distributed in any form whether by way of fax, email, oral or otherwise, in whole or in part without the express and prior written consent of Liontrust.